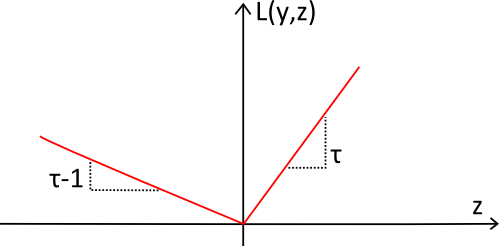

A loss useful for quantile regression. Penalize undershoot or overshoot one side than the other side.

So it may look like this:

For 𝜏=0.1, we would expect the model to underpredict 90% of the time and overpredict 10% of the time. And now we have already bridged the gap to distributions: This is equivalent to the 10% quantile.

Reference:

- This blog: How I made peace with quantile regression